Where Home Prices Are Falling Most Precipitously

The U.S. looks to enter its first major housing downturn in over a decade with some markets holding up better than others

This week U.S. mortgage rates reached their highest level since 2008 with the average 30-year fixed rate mortgage sitting at 6.3%.[1] This has helped to slow record single-family home appreciation that was up 43% over the pandemic.[2] Rising housing prices combined with borrowing rates that haven’t been seen in almost 15 years, have started to sedate America’s previously red-hot housing market.

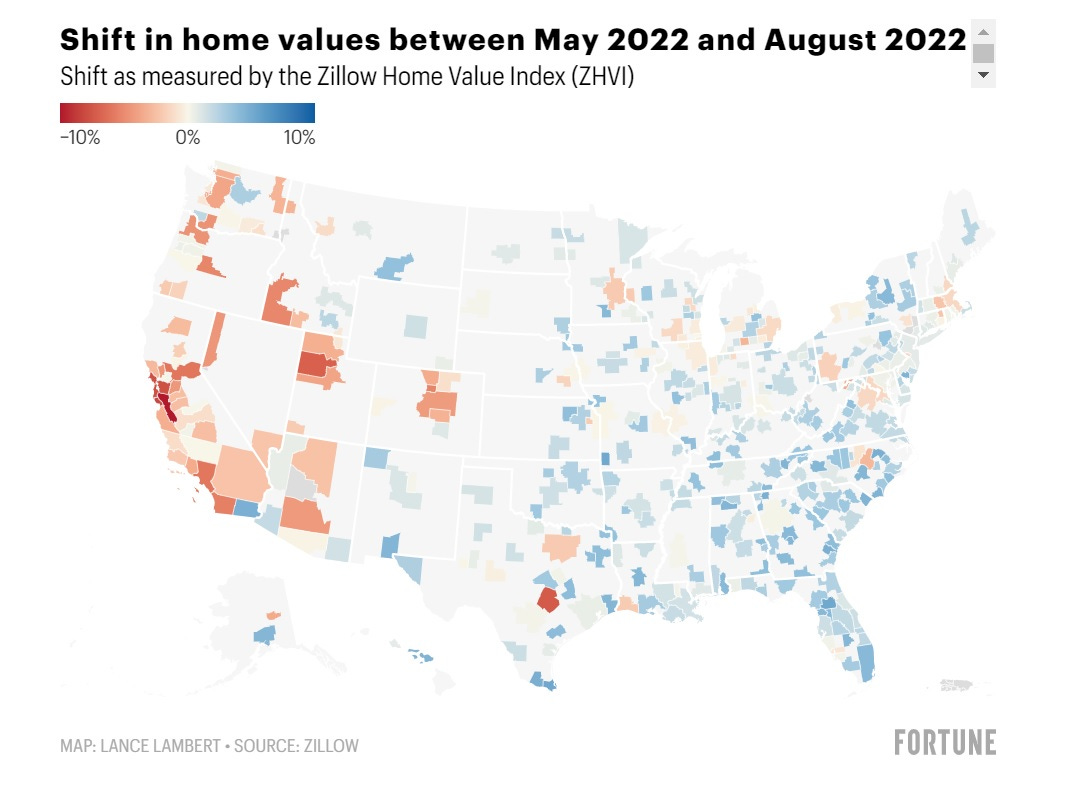

The housing correction is not taking place uniformly across the country. Across 896 major regional markets, 117 markets had home values that fell between May and August 2022.[3]

The price drops have been most acute in high-cost and tech-driven cities like San Francisco and San Jose, with prices falling 7.4% and 4.3% respectively in each market. Though, pandemic boomtowns such as Austin and Denver, where prices have dropped 7.4% and 4.3% respectively, have not been immune to the cooldown in the housing market either.

While prices have fallen in the short-term, recent drops have done little to put a dent in single-family housing gains that were fueled by the low interest rate environment borne out of the pandemic and excess savings that households built up over that time. While housing values in Boise contracted 5.3% during the summer, prices are still up 48.6% compared to where they were in March 2020.

The pressing question is, where do housing prices across the board go from here and how will home values fluctuate either to the upside or downside in different locales around the country? Homebuilder sentiment in September fell for the ninth straight month and reached its lowest level since May of 2014, with the exception of the momentary tumble the index experienced during the depths of the pandemic.[4]

Home values still seem to be rising in low barrier to entry markets where single-family homes are typically priced below $300,000.[5] Secondary and tertiary markets such as Birmingham, Indianapolis, and Cincinnati have benefited from this trend. This makes sense as affordable markets should prove to show greater resiliency as borrowing costs rise and more people do not have the financial wherewithal to support higher levels of debt service.

A new variable that has not had to be accounted for in previous housing downturns, was the proliferation of investors buying up single-family homes over the past few years. It was estimated that investors purchased 24% of all single-family homes nationwide in 2021 up from about 15% in 2012.[6] In states like Florida, Nevada, Vermont, and Washington investor purchases doubled or more from 2020 to 2021. In Nevada investor purchases made up 30% of all single-family home acquisitions in the state in 2021.

It is apparent that investor purchases played a large role in driving up housing prices in the aftermath of the pandemic at record rates. The quick expansion of sophisticated investor groups buying up swaths of single-family homes that have historically been purchased by families is something that a growing U.S. housing market has never had to deal with on the way up. What will this look like on the way down?

Investor groups usually have access to a wider range of capital providers than a conventional homebuyer. They have access to lines of credit that allow them to purchase homes on an all-cash basis and without having to wait to be approved for a 30-year mortgage. This allowed investor groups to purchase homes below market value due to their ability to close quickly and without any contingencies. These groups generally then refinance into a traditional mortgage post-closing.

I suspect that as borrowing costs continue to rise and capital that was easily available over the past 13 years starts to dry-up, investor groups will have a harder time accessing the cash they need to keep purchasing properties in the same way they have been over the latest housing bull-run.

This may magnify the woes for the single-family housing market on the way down. Many of the buyers that were there to prop prices up over the past few years no-longer have viable business models that work in a tighter monetary policy environment. The lack of investor groups purchasing single-family homes may especially be felt in pandemic darling markets where these types of buyers came swarming in with pockets full of cash over the past few years. Many of these markets, particularly in the Sun Belt, were also the worst hit markets during the housing crash that precipitated the 2008-09 financial crisis.

I doubt that this housing slump will come close to rivaling the last elongated real estate downturn almost 15 years ago. The increase in borrowing standards that the post-crisis autopsy brought about means that homebuyers in the latest housing run-up are better able to weather a sudden job loss or salary reduction compared with precrisis borrowers. Though, a housing boom that was fueled by easy-money policies and effortless access to capital can end just as quickly as it started once the spigot turns off.

Have feedback, always feel free to email me at atannenbaum@thedeanlicos.com or DM me on Twitter @Adam_Tannenbaum.

[1] https://www.bloomberg.com/news/articles/2022-09-19/here-s-how-much-a-new-monthly-mortgage-payment-has-surged-in-10-us-metros

[2] https://fred.stlouisfed.org/series/CSUSHPINSA

[3] https://fortune.com/2022/09/20/home-price-correction-spreads-this-interactive-map-shows-if-your-local-housing-market-is-impacted/

[4] https://www.cnbc.com/2022/09/19/more-homebuilders-lower-prices-sentiment-falls-for-ninth-straight-month.html

[5] https://www.marketwatch.com/story/home-values-fell-in-august-the-largest-monthly-decline-since-2011-some-cities-see-house-values-drop-by-3-11663686588

[6] https://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2022/07/22/investors-bought-a-quarter-of-homes-sold-last-year-driving-up-rents