Multifamily Cap Rates Don't Make Sense

3% and 4% Cap Rates Don't Add Up in a Rising Interest Rate Environment

As the 10-year treasury looks to tick above 3% in the not-so-distant future, cap rates across most property types keep compressing. This is particularly true for multifamily assets.

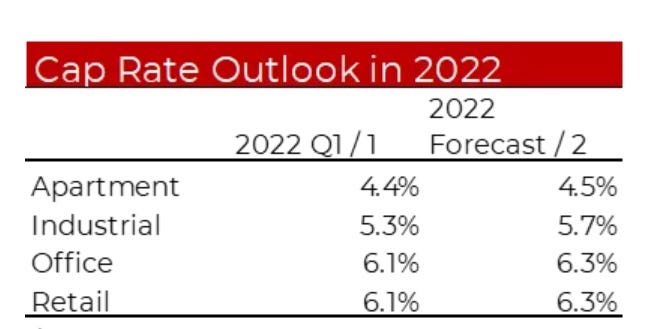

While the average 30-year fixed rate mortgage was about 5.1% as of the end of the week of April 29th, the risk-premium, calculated by subtracting nominal cap rates by the 10-year treasury yield, continues to flatten for multifamily assets.1 With the average multifamily cap rate projected to run at 4.5% in Q2 2022, it hardly makes any sense that assets are continuing to trade at unleveraged yields that are close to or below their financing costs.

For example, let’s say you have a multifamily property that sells for $1M and spits-out $50,000 in Net Operating Income (NOI) per-annum. Trading at a 5% cap rate (unlevered cash-on-cash yield). The buyer then goes out and gets an agency mortgage amortized over 30 years, with a 5% interest rate, at a 75% Loan-to-Value ratio (LTV). Fannie Mae is currently pricing multifamily loans at about 5%.2 The annual debt service on this loan would be a tick under $48,800, leaving little-to-no margin for error.

The dangerous assumption that many buyers are making is that they will undoubtably be able to raise rents that at a minimum keep track with inflation. This is understandable when you look around and see markets like Tampa and Las Vegas recording 28% and 24% rent increases per-annum respectively.3 Though, what makes buying properties at low cap rates in a rising interest rate environment particularly perilous, is both the stagflationary and refinancing risk.

The U.S. economy contracted in Q1 2022 by 1.4% while inflation continued to tick higher, with consumer prices rising 8.5% in March.4 While private demand grew 3.7% in the first quarter and consumer spending rose 2.7%, the GDP downtick shows how there is a fine line between economic prosperity and distress. This is especially true when you factor in ongoing geopolitical risks, arguably the main driver of higher inflation.

Stagflation means that an economy displays slow growth while prices continue to raise at unsustainable levels.5 In previous stagflationary periods, the Federal Reserve had to put the economy into a self-induced recession by raising interest rates in order to tame rising prices. What this generally meant for real estate was severely higher borrowing costs leading to reduced buyer demand.

This was coupled with lower spending capacity for renters, resulting in curtailed pricing power for landlords, meaning lower rents and NOI. This would debunk the rationalization that buyer’s use to justify low cap rates that are close to what they are paying in borrowing costs. Owner’s being able to raise rents and NOI in the future. This forced owners to dig into their own pockets to keep their property’s operations afloat or into fire sales if they could not.

Conor Sen from Bloomberg did a nice job of outlining how stagflation is already effecting the single-family housing market in this article.

Now let’s say The Fed is able to successfully raise interest rates, avoid economic stagflation, and execute a smooth landing, bringing prices down without causing a recession. In this scenario higher interest rates also mean higher borrowing costs for real estate operators. This would be combined with lower inflation, taking away pricing power from landlords, like in the stagflationary scenario.

Lower rent growth in addition to higher interest rates means that anticipated NOI growth will skew downward. The concern in this situation is that when owner’s go to refinance their properties, higher interest rates along with lower income will not allow their assets to support the debt amount that they need to payback their old loans.

While many landlords may try and sell their property to get out of this predicament, they will probably be met with potential buyers that face a similar issue. Wanting to offer a higher price, they can only afford so much because banks are underwriting the amount of their potential acquisition loan to the lower NOI of the property and to higher interest rates. The fear here is that many owners who have overleveraged their assets over the past 30-years to take advantage of accommodative monetary policy, won’t be able to payback the principle on their loans when it comes due. This could clearly have a cascading effect that permeates other parts of the economy.

Have feedback or disagree with what I am saying? Always feel free to DM me on Twitter @Adam_Tannenbaum or email me at atannenbaum@thedeanlicos.com.

https://www.marketwatch.com/story/after-rising-at-the-fastest-pace-in-40-years-mortgage-rates-level-off-but-buyers-shouldnt-hold-their-breath-for-rates-to-move-down-11651154907

https://www.commercialloandirect.com/apartment-interest-rates.php

https://www.realpage.com/analytics/apartment-demand-occupancy-and-rents-jump-to-new-highs-again-in-1st-quarter/

https://www.wsj.com/articles/us-economy-gdp-growth-q1-11651108351?mod=world_trending_now_article_pos2

https://www.wsj.com/articles/rumors-of-stagflation-economy-gdp-first-quarter-white-house-inflation-joe-biden-11651179612